Sessions at the forum had a strong focus on the so-called ‘talent factor’, those bright young students who are being groomed to become the next generation of scientists, technology developers, supply-chain specialists and CEO’s of multi-national companies.

The future, it seems, is downstream and upstream from the farm, as the fastest growth in Africa’s food system is expected to occur in the supply of inputs and in the “post-farm segments” of the supply chain. David Tschirley of Michigan State University suggested that African universities with agricultural faculties would need to make an institutional “double pivot”, which means that they will have to shift from serving public sector to private sector clients and from on-farm technologies to post-farm segments of the food system.

David vs. Goliath

According to Lulama Traub of Stellenbosch University, the mega-trends that shape the African continent include rising global food and energy prices and rising income and urbanisation, though evidence suggests an increasing concentration of wealth. While this will cause a shift in demand for food, the fact that the non-farm sector will not on its own be able to absorb Africa’s future work-seeking population, means that there will be pressure on agriculture to create employment.

In the light of such heavy expectations of agriculture, who should be the agricultural producers?

At a session titled “David vs. Goliath: The revolution in Africa’s farm structures”, aimed at identifying the trends and constraints affecting agriculture, Antoine Ducastel, CIRAD research fellow at Pretoria University’s research on large-scale land investments in Africa showed that investments are made by private investors with market-driven strategies from Western countries and countries rich in capital, but with poor land and water resources, who invest in land to secure supplies of agricultural commodities and to get around volatile commodity markets. Contrary to popular perceptions, China remains a small player in land acquisitions in Africa, while investors from South Africa are becoming more engaged, especially in Southern African countries.

Because of a high rate of failures and the difficulty of implementing projects in Africa’s “uncertain institutional environment … [with a] lack of markets and financial services, high settlement and transaction costs”, land investments had been slowing down since 2010, but the trend is still upwards. Of all the hectares acquired since 2010, only 1,7% is operational and producing. The only investment models that seem to be successful are “nucleus estate models” (based on small-scale contract or outgrower schemes) and “agribusiness estate models” (where big agro-food companies buy land and farm to secure supplies of commodities and integrate production in their own value chains).

As a consequence, investor strategies and business models are being transformed and increasingly integrated into closed value chains, but few inclusive business models were found. The major impacts on agrarian structures of affected countries have been the corporatisaton of agriculture, concentration and industrialisation in agriculture and the proletarianisation of agricultural societies.

Ducastel said the question that remained unanswered was how local actors and communities could benefit from these transformations and added that he found few cases with a positive social and economic effect. He also found a lack of long-term thinking among policy makers and investors about alternative development trajectories and an increasing shift towards a large-scale development paradigm.

Not just foreigners: the rise of urban business and bureaucratic elites

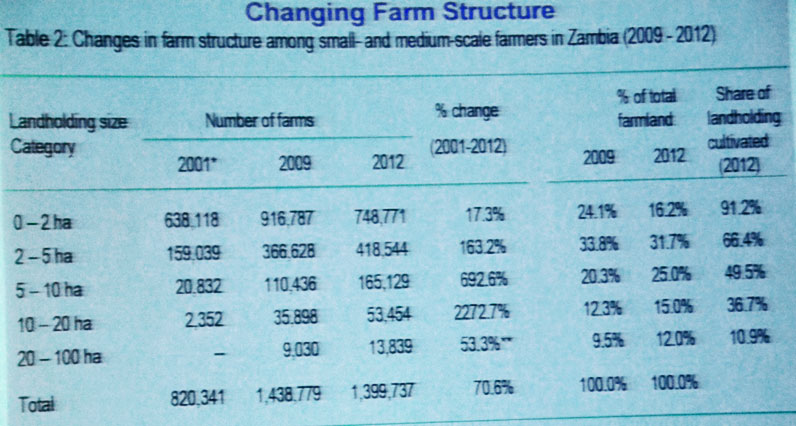

In the same session, Milu Muyanga of Michigan State University showed an interesting table of the changing structure of small and medium scale farming in Zambia from 2009 to 2012.

(click on image for full size)

Besides the fact that the area of farm land has decreased by about 30% since 2009, the figures show that farms are getting bigger, but that a smaller proportion of the bigger landholdings are cultivated. Muyanga says the medium-scale farmers (owning 10 – 20 ha) are the fastest growing group. He found that most of them were civil servants and professional people who used money made in other sectors to buy more land. The majority of them had higher education and also inherited land from their fathers.

His comparative research found that there were more conflicts taking place over land than in the past, especially in Kenya, probably because the landholdings were becoming smaller because of increases in population. The land that was still available is often remote and there is a lack of infrastructure and services.

African consumer growth and the large-farm model

During a session about the rise of an African consumer class Paula Disberry of the South African retailer, Woolworths, said that retailers needed a value chain that can service their needs for scale, quality and consistency. They have big, powerful brands to protect and cannot risk disappointing customers. At the same session, M.D. Ramesh, Olam International’s regional head for South and East Africa, said that African countries annually import $81 billion’s worth of products, of which $32 billion is spent on imports of maize, rice, wheat, sugar and edible oils, because the agricultural sector did not received the support it deserved. He reckons it would take 100 companies like Olam (with a market capitalisation of almost $6 billion) and $55 billion to resuscitate small farms and transform agriculture in Africa.He did not say what this transformation would entail, but one of his Olam colleagues suggested that, while the ‘David model’ is an emotive model, it is more expensive and capital-intensive and this multinational at least favours ‘Goliath’.

Amelia Genis attended Ifama as an agricultural journalist, but wrote this blog in her personal capacity. She is a PhD student at the Institute for Poverty, Land and Agrarian Studies (PLAAS) at the University of the Western Cape, South Africa, which is the Southern Africa hub of Future Agricultures.